Investor’s Take on the NAR Housing Data

I often am out there talking to my compadres in the real estate investing world, as I find it helpful to not only look at reams of data but also talk to other people within my industry. I have also discovered over the years that very few investor types actually network with each other. Usually it is the old school mentality that they might steal my deal or idea or maybe because we have become so accustomed to beating each other up on properties that we have some underlying resentment towards each other. In my younger years my only reference was some old school developer types that were (probably still are) highly secret about anything they are doing. To put those fears aside I have found that in today’s technology day in age it is actually very difficult to get any proprietary deals, and people pretty much see everything if they wanted to look. I’m not saying that proprietary deals don’t exist but ironically enough they are usually sourced through your network. I have also found that as I network more I am exposed to new ideas or variations on my ideas. And I’m not talking the MLM (multi-level marketing) networking, I am talking about making genuine connections and building friendships and relationships.

Challenge: When was the last time you reached out to someone and had some coffee or lunch? Go do that, I promise you it will be more worthwhile than the cost of the lunch.

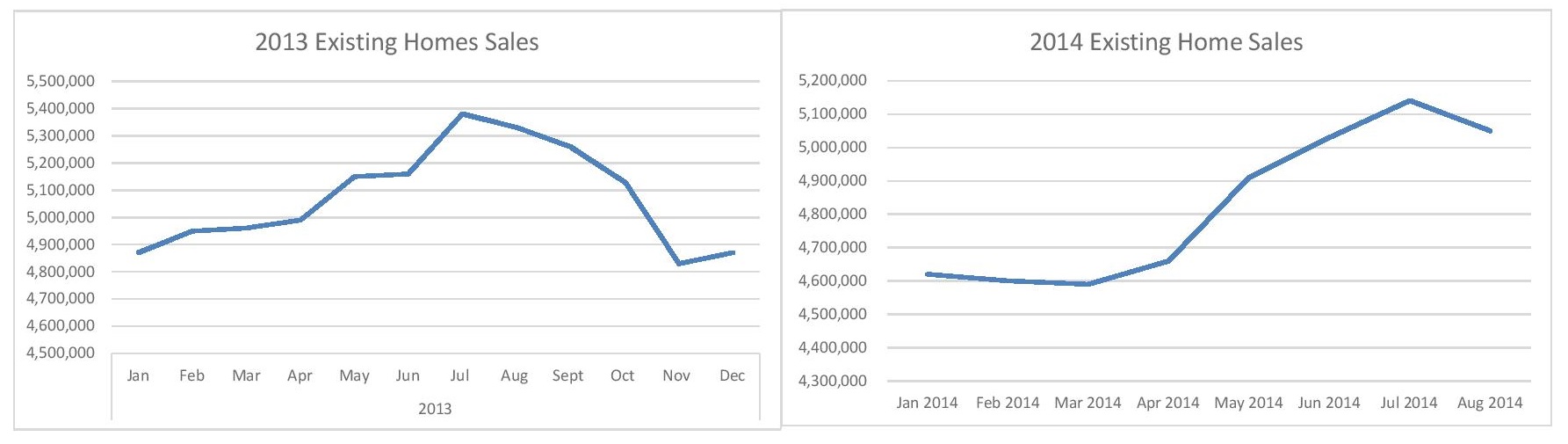

Back to my point, my fellow investors don’t really need a NAR report to tell them what is going on in the market as they are living the data on a day to day basis and what we are seeing is the regression to the mean on these DOM and a slight pull back on pricing. Their sentiment is that the market in Sacramento and most of the West coast is much softer these days. Given the overall lack of distressed “good” deals and buyers being even more picky than usual. The buyers that watched Blackstone (Invitation Homes) come in and buy up several thousand homes for rentals helped stimulate a 15-20% market appreciation (Which is good if you own a house, bad if you are looking to buy one). Well those buyers feel like they have missed out on getting an affordable house. As a result the prices are much higher and rates are slightly higher (4.19% 30 year fixed currently) so they are holding out and looking for that perfect house and some are actually being unrealistic but there is nothing in the market to externally motivate them.

My take on the market is we are seeing a lot less distress in the market. The investors, me included have been picking the low hanging fruit “Deals” for several years now. With the lack of low hanging fruit the competition has been forced to do 4 things.

1) Move to areas with more deals/less competition

2) Accept lower and lower returns

3) Find a new niche or value add component (additions, new builds, commercial)

4) Close up shop and move on (take their ball and go home)

The fact that we are seeing less distressed properties being sold. The bidding wars coming to an end, plus the DOM are on the rise this business gets less and less profitable by the day. I have been seeing many of my competitors do some variation of all 4 of those options.

DOM (Days on Market)

I’ve mentioned it a few times in a couple of blogs. But, why do the DOM matter that much? As an investor it’s almost just as beneficial to sell a property quickly as it is to sell it for maximized price. The reason for this is a lot of investors are looking at the annualized rate of return.

Scenario 1) If I invest in a house for 100k and sell it for 120k in 3 months my profit is 20k and my annualized return is 80% (20% x 4)

Scenario 2) If I Invest in that same house for 100k and sell it for 130k in 6 months my profit is 30k but annualized return drops to 60%. (30% x 2)

Which of those would scenarios you rather?

Well to me both are good options but it really depends on the underlying objectives and market conditions. If you have 5 million dollars and you can only buy 2 million worth of good deals because of lack of inventory. Then I would lean towards the maximize profits because you can’t source enough deals (spend all your money). If the market has a ton of deals that fit your pricing matrix then you go for lower return but higher volume as the velocity of that money is much higher at 4x vs 2x.

What usually happens is a combination of those two, you can source a certain amount of deals in this environment and you are typically holding back a little just in case that home run deal comes along. But given the opportunity to make a quick exit you will usually take it . Now the flip side of that is the hold times start creeping up there the investor mentality is to cut bait given a 6+ month hold time. They feel like they are chasing a bad return and would almost rather cut the pricing to break even and just be done with it in hopes their next deal is better than that one.

Less properties = Less competition

Now that we are seeing less distressed properties what does that mean for the future. My take on it is that it is a good thing. The bigger funds with massive overhead have to move on to greener pastures or get bogged down chasing too few deals. The midsize funds battle it out and lean up, doing more with less and take some hits on a few properties as the market adjust to an environment where the buyers rule to roost. This will drive some of the other midsize funds to move on as well. The mom and pops in general will take the biggest hit as they typically will have all their money in 1 or 2 deals and if they take losses on those then they will quickly exit the market.

There is still levels of distress coming down the pipeline but the banks have gotten better at how they dispose of it and with levels of competition lower there will be some opportunity for a patient but well-funded investors. As the vacuum of the competition leaving the markets will allow for some deals to slip through the cracks.

But and this is a big but, since that low hanging fruit is gone all of the investments should be based on solid fundamentals not speculation of the market. I’ll go more into the fundamentals in the future.

God Bless and go network with someone

Jake