Supply and demand is in my opinion the single largest factor in determining real estate values. I know we could get into affordability, interest rates and jobs. I think those are all important but the single largest factor to me is: supply and demand (people want more properties than are available, prices go up and not enough demand for properties prices go down)

There are different forms of supply and demand in the market today. The reality is that over the last 4 to 5 years we have seen a substantial amount of distress in the markets. By distress I mean forced sales, foreclosures, short sales, and tax sales. As a result we have seen a lot of demand from investors on both the individual and institutional levels. The homeowners have been doing their small part of this as they are absorbing the properties in post distress state via equity sale. However a large portion of this distress has just been pulled off the market in the form of rentals. (Invitation homes, Homes 4 rent, Blackstone, Colony)

In those last 4 to 5 years I have been on the forefront of buying up those distressed properties and been in a unique position to watch the markets transform from the driver’s seat. But now in the last year or so I have seen a shift in the market. It has been a complex shift.

1st) is the amount of distress in the market has waned (less foreclosures).

2nd) is we have recovered a significant portion from the bottom. These range by area but some are 50-80% recovered and in fact some areas have new record values.

3rd) is because of 1 and 2 we are seeing less investor activity. (Not as many deals and not as good of a price, no need to invest)

What I am seeing as a result of that is markets that were dependent on investors driving demand have cooled off, and as a result it’s left to the “regular” equity sales to sustain those levels.

The problem I’ve identified is that in markets that have been stimulated by investor demand for flips and rentals could be at risk for a pull-back in pricing because they don’t have the underlying fundamentals necessary to sustain that recovery. (The demand reduces, the supply increases and prices fall)

Does that mean the jig is up and we as investors need to just go home now? That really depends on what your expectations are on returns, what your long term goals are and where you are located.

To me the answer is no, but I am also more cognizant about about where I look to invest and at what margins I am willing to invest. As I prefer to be in and out of markets “flips” I look to markets that can sustain growth based on factors outside of investor demand. Which to me boils down to population.

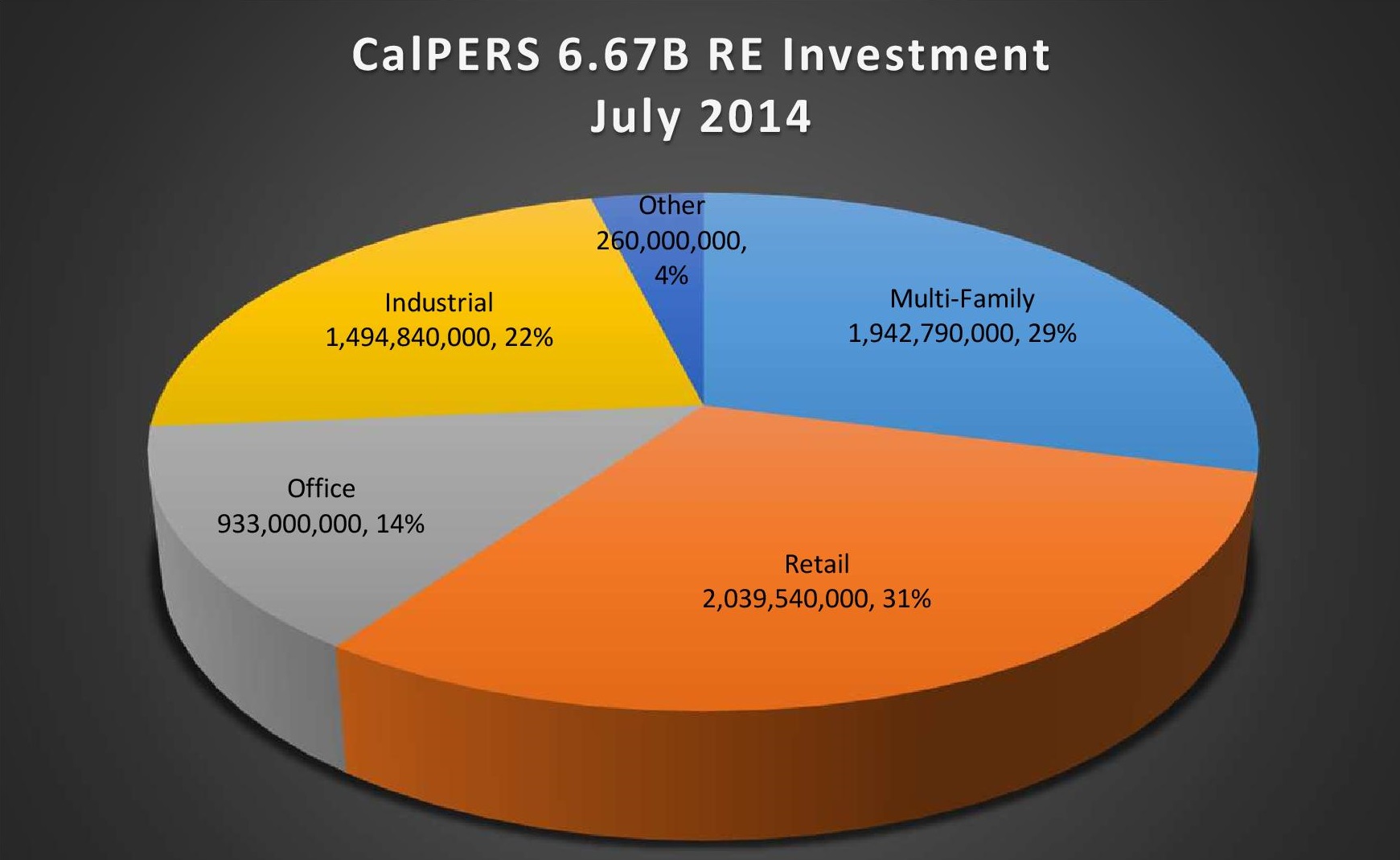

Below I have attached a chart of the top 10 metro areas of over 1 million that have seen the largest percentage of growth from 2010-2013.

Firebird Investment Group 2014

As you can see from the highlighted section, 4 out of the top 10 are in Texas. With over 1M new residents just in those 4 metro areas which is more than the top 6 California metro areas combined. My interpretation is that there is more demand just based on the simple population increase.

There are other factors I look at beyond just population growth. Like new housing starts, unemployment rates, affordability but this is one of the most crucial components to driving prices. More demand = higher prices.

God bless and looks like everything IS bigger in Texas,

- Jake